Europe Doesn’t Have a Capital Problem. It Has a Competitiveness Problem.

Rethinking the Venture Narrative Through First Principles

There is a growing consensus in European venture and policy circles: Europe produces excellent founders and companies, but lacks sufficient mid and late-stage capital. The proposed solution is equally clear, mobilize institutional capital, particularly pension funds, to close the gap.

It is a compelling narrative. It is also a convenient one.

Because if the problem is capital, then the solution is straightforward: allocate more of it. No difficult trade-offs, no uncomfortable structural reforms, just better coordination and a bit of political will.

But the simplicity of the diagnosis should give us pause.

If the opportunity were as obvious as it is often presented, high-quality companies, underfunded at scale, with strong risk-adjusted returns, then capital would already be flowing.

Pension funds, sovereign wealth funds, and global LPs are not structurally incapable of identifying return. They deploy across geographies, asset classes, and cycles and they in many cases scour the world to do so.

So the question is not whether Europe needs more capital. It is:

Why has capital not already moved in the way the narrative assumes it should?

Answering that question honestly requires stepping away from slogans and returning to first principles. And when we do, the issue begins to look less like a funding gap, and more like a competitiveness gap.

The Capital Gap Is an Outcome, Not an Input

It is tempting to treat capital as the primary lever in venture ecosystems. Add more of it, and the system improves. But venture does not operate like a machine where inputs and outputs scale linearly.

This is not an argument against increasing capital per se, but against mistaking capital for competitiveness. Because capital is not a catalyst in isolation. It is a response to expected outcomes. And where outcomes are uncertain, capital doesn’t disappear, it becomes selective.

Markets are not perfectly efficient, but they are rarely so inefficient that large pools of capital systematically ignore obvious, repeatable return opportunities. If European growth-stage venture consistently offered superior risk-adjusted returns, global capital would not need encouragement, it would already be present, and in size.

The persistence of the so-called “capital gap” suggests something else is at play.

The shortage of capital is, at least in part, a reflection of underlying conditions that make deploying that capital less attractive than the narrative implies.

This is where the idea of a conviction gap becomes more useful than a capital gap. Capital is available. What is missing, in many cases, is the level of conviction required to deploy it at scale and over time.

Conviction, however, is not created through policy statements or industry reports. It is built through consistent outcomes.

If the Returns Were There, LPs Would Already Be There

This is the question that tends to sit quietly in the background, rarely asked out loud:

If European venture represents such a compelling opportunity, why are large institutional LPs not already allocating more aggressively?

It is tempting to frame this as a failure of imagination or risk appetite. It is neither.

Pension funds and institutional investors are fiduciaries. Their role is not to support narratives, ecosystems, or policy ambitions. Their role is to generate the best possible risk-adjusted returns within the context of a diversified portfolio.

And many are already invested in venture, just disproportionately elsewhere.

They allocate significant capital to US venture not because of storytelling, but because of:

- Depth of the market

- Consistency of top-decile outcomes

- Scalable fund platforms

- A more predictable path from company formation to exit

This is not a philosophical preference. It is a portfolio construction decision.

Capital is not absent from Europe because LPs are uninformed. It is measured because they are doing their job.

Which leads to a less comfortable but more useful conclusion

If capital needs to be persuaded, nudged, or politically encouraged to participate, it is usually a sign that the underlying conditions are not yet compelling enough on their own.

More bluntly: pension funds don’t need a narrative. They need a reason.

What Founders Actually Optimize For

At the center of this discussion sits the only group that ultimately matters (and who in the midst of all of this seems somewhat overlooked): the founders.

Much of the current narrative assumes that founders would prefer local capital if more of it were available. It is an appealing assumption. It is also, in many cases, incorrect.

Founders optimize for probability of success.

That includes access to capital, but also access to markets, talent, expertise, and future financing. Geography is in all that somwhat secondary to outcomes.

Raising from a leading US fund continues to function as a form of global validation. It signals quality to future investors, employees, and customers. European investors, despite meaningful progress, often still follow that signal rather than set it.

But the difference goes beyond signaling.

The US offers something Europe still struggles to replicate: a truly unified market. For a founder, this translates into faster scaling, more predictable expansion, and fewer structural obstacles. Europe, despite its size, remains fragmented in ways that directly affect execution.

In that context, a US investor is not simply providing capital. They are providing:

- A bridge into a large and coherent market

- A network that accelerates commercial traction

- A level of operational support built over decades

There are also differences in how venture firms engage. In the US founders frequently encounter senior, experienced investors early in the processes. In Europe, initial interactions are more often outsourced to relatively inexperienced juniors (same type of screening you would see in a buyout, except in a buyout the juniors are using spreadsheets to screen opportunities not wasting founders’ time). This affects both speed and substance.

And then there is the question of proactivity. US funds track companies globally and engage well before capital is needed. By the time a round is raised, they are already part of the story. European funds, more often, arrive later.

These differences accumulate.

Finally, there is something harder to quantify but impossible to ignore. For many founders, the US remains a benchmark, a place to test ambition at scale. Not necessarily a permanent destination, but a proving ground.

While an uncomfortable truth, that matters more than policy narratives and European VCs tend to acknowledge.

The Structural Reality: Friction Is Not Neutral

Europe’s structural challenges are well known. They have been documented extensively and debated repeatedly. But they are often treated as background noise rather than primary drivers of venture outcomes.

They are not neutral.

A fragmented single market slows down scaling. Regulatory divergence increases operational complexity. Language and cultural differences introduce friction in go-to-market strategies. Tax regimes can, in some cases, disincentivize risk-taking or penalize success. Talent mobility, while improving, remains uneven.

Individually, these are manageable constraints. Collectively, they shape outcomes.

For venture-backed companies, where speed and scale are critical, these frictions translate into:

- Longer paths to product-market fit across regions

- Higher capital requirements

- Greater execution risk

- More complex exit pathways

Which leads back to capital allocation.

When the path to scale is more complex, capital becomes more cautious, not more abundant.

This is the critical link: structural friction does not just slow companies down, it directly affects returns. And over time, that feeds back into capital allocation.

The “Small Is Beautiful” Illusion

Within European venture, there is a persistent belief and subsequent ‘shouted from the rooftops’ that that smaller, more specialized funds are inherently superior. It is an attractive idea, focused, disciplined, close to founders.

It is also, in many cases, disconnected from reality.

True specialization requires sufficient deal flow, deep domain expertise, and the ability to support companies over time. In many European markets, the opportunity set is simply not large enough to sustain this model at scale. In that context, many funds are not truly specialized, they are constrained.

The result is a proliferation of subscale funds that position themselves as specialists but operate more like generalists with limited reach.

At the same time, global data increasingly points toward the advantages of scale in venture:

- Access to the best deals

- Ability to follow on through multiple rounds

- Stronger platform capabilities

- More consistent exposure to outliers

Large, multi-stage platforms are not successful by accident. They are built to capture the full lifecycle of value creation.

Fragmentation at the fund level mirrors fragmentation at the market level and both have consequences.

A Behavioral Gap That Is Harder to Discuss

Beyond structure, there is also behavior.

European venture has matured significantly over the past decade. But it remains, in many ways, a younger ecosystem. That shows up in how risk is approached, how firms are built, and how incentives are structured.

US venture is, at its core, an exercise in capturing extreme upside. It tolerates failure because the winners dominate outcomes.

European venture often leans more toward risk management:

- Greater focus on downside protection

- More emphasis on valuation discipline (also a function of smaller subscale funds)

- A tendency to avoid outlier risk

This is not inherently wrong. But it produces different outcomes.

There is also a question of intensity. In highly competitive ecosystems, venture is a performance-driven business. Capital is reallocated quickly, and underperformance has consequences.

Where public capital plays a larger role, as it often does in Europe, the pressure can be different. Stability can become a feature. Over time, it can also become a constraint.

To put it plainly:

Parts of European venture risk becoming structurally less performance-driven than their much larger US counterparts.

And comfort is rarely where outlier returns come from.

When More Capital Meets the Same System

Against this backdrop, the push to mobilize more capital is understandable. But it is not without risk.

If the underlying system remains unchanged, increasing capital supply does not necessarily improve outcomes. It can, instead, amplify existing inefficiencies.

More capital can lead to:

- Weaker selection discipline

- Increased competition for subscale opportunities

- Fund formation driven by access to capital rather than capability

- Political influence over allocation decisions

In other words, it can optimize for activity rather than performance.

And this leads back to a simple but often overlooked point:

No one invests in venture for average returns.

If the system does not consistently produce outliers, or does not consistently capture them, then increasing capital alone will not fix it.

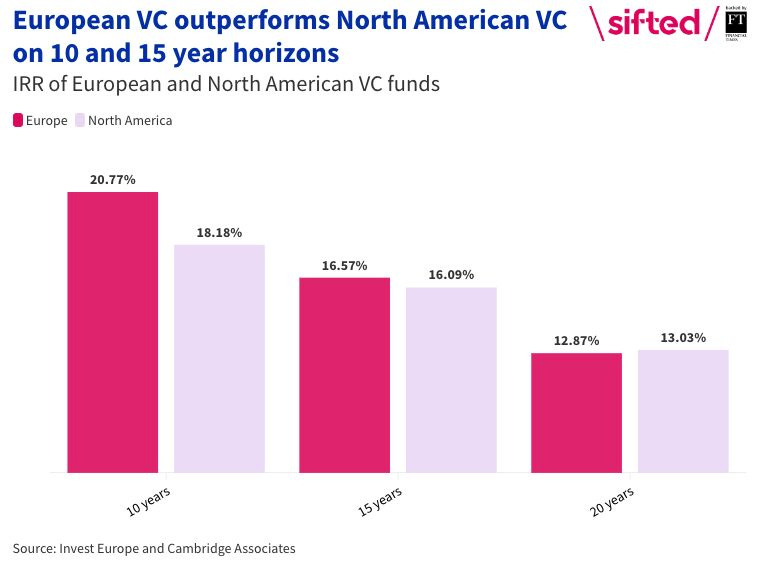

In Europe, ever since Invest Europe published it, we have been very fond of socializing the chart below among investors.

Source: Sifted / FT, data from Invest Europe and Cambridge Associates.

It tells a compelling story , and one we would very much like to believe.

The problem is that it rests on a highly selective dataset.

As David Clark (VenCap International plc) points out, of the 2,733 VC funds raised in Europe (including the UK) between 2010 and 2019, only 88 are included in the Cambridge benchmark. That is just 3.2% of the total universe. In some vintage years, the sample consists of as few as three funds.

In a power law asset class such as venture, that is not a minor technicality. It fundamentally undermines the conclusions.

At best, the data is incomplete. At worst, it is misleading.

This matters, because the chart is often used to support the idea that European venture delivers comparable, or even superior, outcomes.

The reality is that it primarily reflects average returns across a highly selective sample. And no serious institutional investor allocates to venture for average returns.

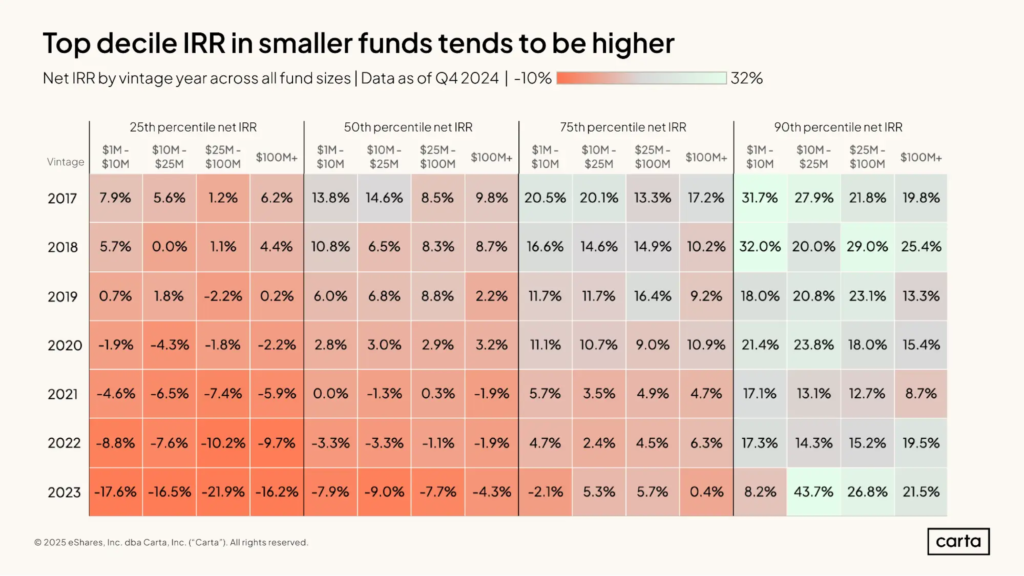

A more relevant lens is how outcomes behave across the distribution:

Source: Carta, VC Fund Performance 2024

While not directly comparable, the pattern is clear. In a power law industry, outcomes are driven by the top decile.

And when investors optimize for consistent access to those outcomes, the allocation patterns we observe begin to make more sense.

By the way, the whole report from Carta is full of great data and well worth a read – Peter Walker , maybe you have some data on pooled IRRs for US VC in quartiles?

What Would Actually Need to Change

If Europe wants a globally competitive venture ecosystem, the focus needs to shift from capital to conditions.

That means addressing the fundamentals

- Making the single market function in practice

- Reducing regulatory friction in ways that affect real companies

- Aligning tax systems with entrepreneurial incentives

- Enabling talent mobility at scale

It also means evolving venture itself

- Becoming more proactive

- Building deeper domain expertise

- Engaging more directly at senior levels

- Focusing on value creation, not just capital deployment

- Not treating it as a subset of buyouts

None of this is easy. Much of it is politically uncomfortable. Some of it will lead to uneven outcomes across countries. Some of it will increase inequality.

But that is the nature of competitive systems.

Capital Follows Conditions

Europe does not lack talent. It does not lack ambition. And it does not lack capital in absolute terms.

What it lacks, in parts of the system, are the conditions that consistently translate those inputs into globally competitive outcomes.

Until those conditions improve, the belief that more capital will close the gap risks becoming circular: capital is needed because outcomes are lacking, while outcomes remain constrained by the very factors capital alone cannot fix.

In the meantime, outcomes will continue to reflect those underlying conditions. The most ambitious founders will, in many cases, still gravitate toward the US, not necessarily out of preference, but because it offers a clearer path to scale, capital, and global validation.

European VC will remain active, particularly in the very early stages, helping to identify and de-risk companies. But too often, that role risks becoming transitional rather than enduring, participating early, only to see later rounds, control, and ultimately value creation migrate elsewhere, mostly the US.

Put differently: without structural change, Europe risks remaining the place where companies are started, but not where they are ultimately built.

Capital does not create competitiveness. It follows it.

What makes this particularly challenging is that much of this is already understood within the ecosystem. Founders, LPs, and even many GPs and likely some policy makers see the same patterns, just not always in public.

Because saying it out loud is uncomfortable. It challenges incentives, narratives, and, in some cases, livelihoods.

Until those realities are acknowledged openly, nothing changes.

Stay Illiquid!

Kasper

This article is provided for informational purposes only and does not constitute investment advice, legal advice, or a recommendation to buy or sell any security, financial instrument, or investment strategy. Nothing herein constitutes an offer or solicitation in any jurisdiction. Any references to investment strategies, market activity, or participants are illustrative and do not imply the availability of any investment opportunity. The content is not directed at retail investors. Where applicable, access to investment-related information is restricted to professional or institutional investors under relevant laws and regulations, including but not limited to Regulation D under the U.S. Securities Act of 1933, the EU Alternative Investment Fund Managers Directive (AIFMD), and the UK Financial Promotion Regime (COBS 4). Views expressed are those of the author(s) and may change without notice.

More Insights

Balentic Edge

Sign up to keep up to date with the latest news and updates.

© 2025 Balentic ApS. CVR: 44034255. All rights reserved.

Privacy Policy | Terms of Service

The Balentic website and Orca are, and are expected to continue to be, under development. Consequently, some of the features described in this Overview and/or on the website may not yet be available or may work differently. Some features may furthermore not be available to all users.