The Operational Era: Finding Liquidity and Value at High Altitude

While the denominator effect has faded, private markets face a new “numerator problem”: a scarcity of exits. In 2026, success will depend on manufacturing liquidity, operational value creation and navigating the bifurcation between AI hype and infrastructure reality.

Editor’s note

This Annual Outlook is a curated synthesis of 2026 investment outlooks from major asset managers, investment consultants and private banks, including Adams Street Partners, Apollo Global Management, Barclays Private Bank, BlackRock, Cambridge Associates, Goldman Sachs Asset Management, J.P. Morgan Asset Management and Partners Group. It identifies the consensus themes, structural tensions and strategic implications for institutional limited partners (LPs). This analysis is not original research, marketing material or financial advice.

Key takeaways

- Liquidity is the new leverage. With traditional exit routes constrained, secondaries and continuation vehicles have shifted from distress signals to essential portfolio management tools, becoming the primary “release valve” for the industry.

- Operational alpha is non-negotiable. The era of “beta-driven” returns – fuelled by multiple expansion and cheap debt – is over. Managers must now generate returns through earnings growth, margin improvement and strategic M&A.

- Real assets are the engine of AI. While software captures the headlines, the immediate investable opportunity lies in the physical infrastructure – power generation, grid modernisation and data centres – required to sustain the AI revolution.

- Private credit is bifurcating. As spreads tighten in the upper middle market, the asset class is evolving beyond direct lending into a broader ecosystem of asset-based finance (ABF) and hybrid capital solutions.

- Private wealth is a structural force. The “democratisation” of private markets is no longer a marketing slogan but a capital reality, driving the proliferation of evergreen structures and altering fundraising dynamics for general partners (GPs).

“We are no longer debating whether private markets matter. The question is how selectively capital should be deployed as liquidity gradually returns.”

Jeff Diehl, Managing Partner & Head of Investments, Adams Street Partners

Introduction

Private markets enter 2026 in a state of suspended animation. The acute anxiety of the “denominator effect” – where plummeting public markets left institutional portfolios overallocated to private assets – has largely subsided.

In its place, however, a more stubborn challenge has emerged: a liquidity drought. While public equity markets have rallied, private market exit volumes remain subdued, leaving LPs with portfolios that are valuable on paper but cash-flow negative in practice.

The consensus across 2026 outlooks is that the industry has reached a pivotal maturity point. The “easy money” era, characterised by falling rates and automatic multiple expansion, has definitively ended.

Partners Group describes the current environment as “investing at high altitude,” where valuations start from a historically elevated base, leaving little margin for error.

Consequently, the focus for 2026 has shifted from accumulation to execution. For general partners (GPs), the priority is returning capital to impatient LPs. For LPs, the challenge is navigating a market where dispersion is widening, and the gap between top-tier managers and the median is becoming an unbridgeable chasm.

The narrative for the coming year is not about the “death of the 60/40” or the supremacy of alternatives, but rather the hard work of extracting value from mature portfolios in a higher-rate, lower-growth world.

Macro and market backdrop

The economic consensus for 2026 is one of resilience tempered by limited upside. Most managers anticipate a “soft landing” or a continuation of modest growth, avoiding the deep recessions feared in previous years.

However, this stability comes with a caveat: the “higher for longer” interest rate narrative has evolved into a “settling higher” reality. Base rates are expected to remain elevated compared to the post-GFC era, fundamentally altering the cost of capital for leveraged strategies.

Private markets are moving from a liquidity drought to a period of selective reopening, where dispersion rather than direction will define outcomes.

BlackRock, Private Markets Outlook 2026

Inflation has moderated but remains a structural risk, driven by deglobalisation, decarbonisation and demographic shifts. This environment creates a bifurcated landscape.

On one hand, the United States continues to demonstrate economic exceptionalism, powered by robust consumer spending and technological innovation. On the other, Europe faces stronger headwinds, with stagnation in key economies like Germany prompting expectations of further monetary easing from the ECB.

Geopolitics has moved from a background risk to a central investment theme. “Economic security” is now a primary driver of capital allocation. Governments are actively incentivising the onshoring of supply chains and investment in critical infrastructure, creating policy tailwinds that private markets are uniquely positioned to capture.

However, this fragmentation also introduces complexity, requiring investors to navigate a world of tariffs, protectionism and diverging regulatory regimes.

Private markets in a whole-portfolio context

The role of private markets in institutional portfolios is evolving from a satellite “alpha booster” to a core component of asset allocation. The rigid binary between public and private assets is blurring, giving way to what BlackRock terms “a new continuum.”

Investors are increasingly viewing their portfolios holistically, seeking the best vehicle – public or private – to access specific themes like AI or the energy transition.

Allocations are shifting. The traditional 60/40 model is being supplanted by frameworks closer to 50/30/20, with private assets comprising a substantial, permanent slice of the pie. This structural shift is driven not just by the search for higher absolute returns, but by the need for diversification in a world where stock-bond correlations have become unstable.

However, this maturity brings new scrutiny. LPs are no longer satisfied with the “illiquidity premium” as a theoretical concept; they demand realised returns. The focus has moved from commitment pacing to cash-flow management.

As Goldman Sachs notes, in an environment where nearly everything looks expensive, active selection and dynamic asset allocation are the only remaining levers for outperformance.

Key structural themes

The liquidity imperative and the rise of secondaries

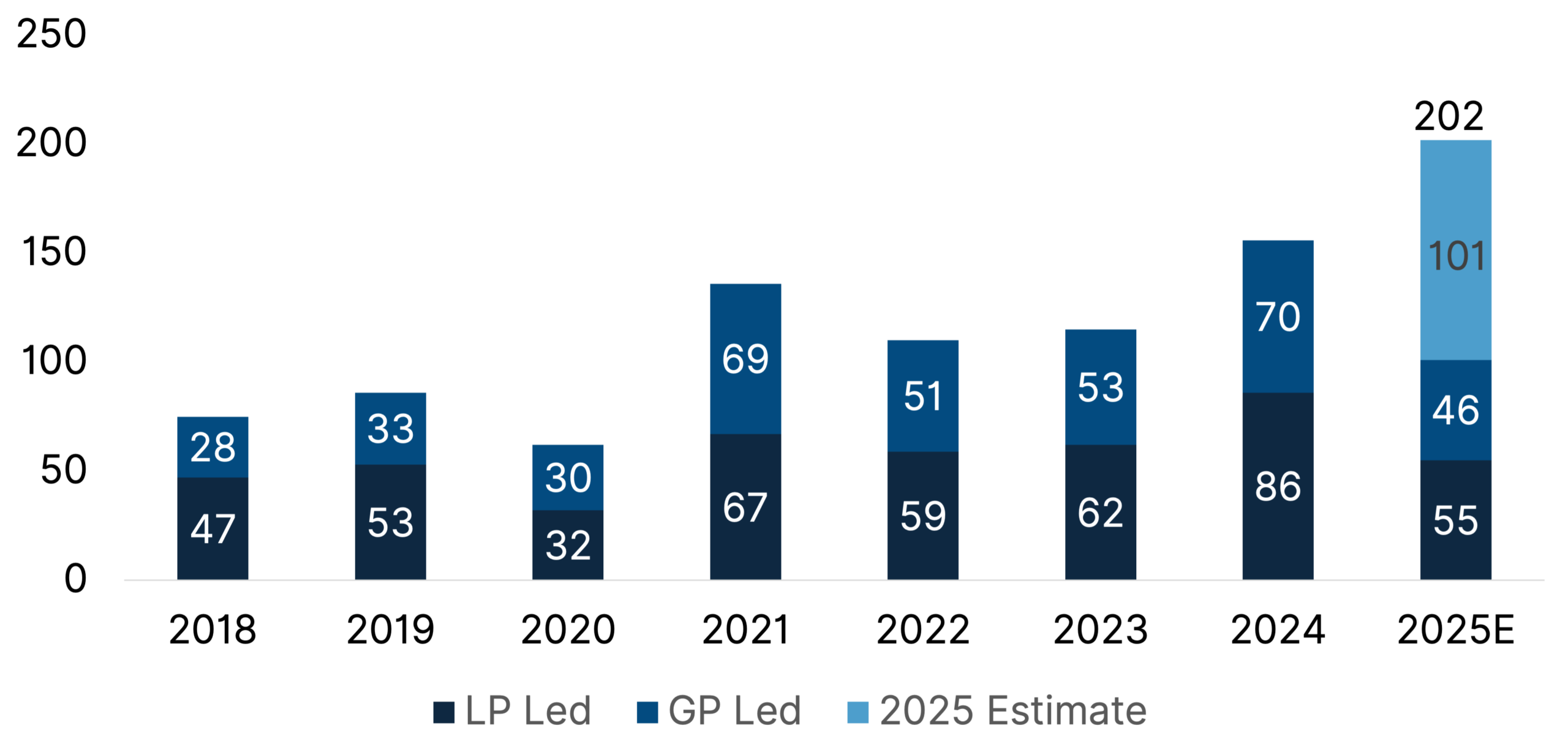

Liquidity has become the scarcest commodity in private markets. With the IPO window remaining selective and M&A activity recovering only gradually, LPs are facing a net-negative cash flow environment. This has transformed the secondary market from a niche distressed channel into a fundamental tool for portfolio management.

LP-led secondaries are being used proactively to rebalance portfolios and generate the cash needed for new commitments. Simultaneously, GP-led continuation vehicles (CVs) have surged, becoming a standard mechanism for managers to hold onto trophy assets while offering liquidity to LPs who need it.

Secondaries have become permanent market infrastructure, providing liquidity and flexibility rather than episodic relief.

Adams Street Partners, Private Markets Outlook 2026

As it happens the economic policies, even allowing for a quasi trade war with China, were on the whole, I think, beneficial for the industry, which also, even if also a beneficiary of public support, weathered the Covid years. In fact, many funds invested in this period of time look set to perform well.

Figure 1: Growth in private markets secondary transaction volume

Expansion of secondary market activity over time, USD bn

Source: UBS, 2025

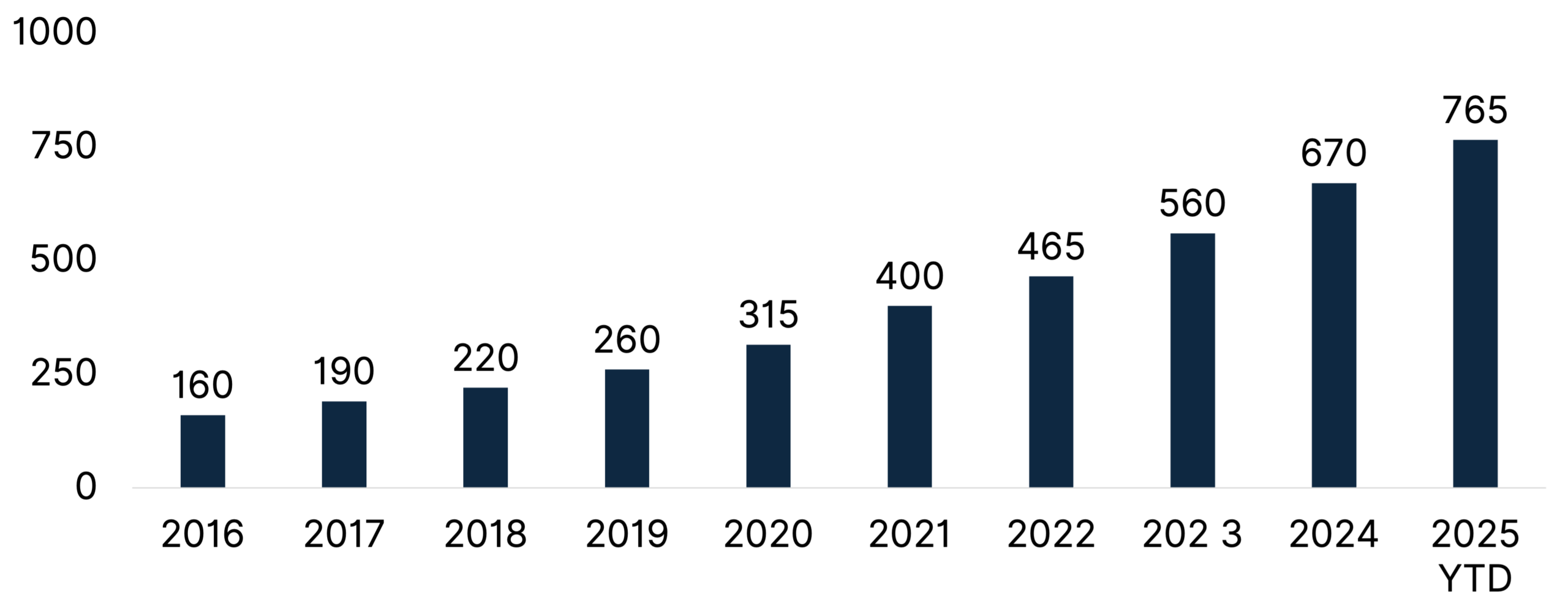

The “Democratisation” of private markets

The entry of private wealth into private markets is a structural shift that is reshaping fundraising. With institutional allocations to private equity nearing saturation, GPs are aggressively courting high-net-worth individuals and family offices.

Private markets are entering their next phase of growth through distribution rather than strategy innovation, as access expands beyond traditional institutional capital.

BlackRock, Private Markets Outlook 2026

Barclays notes that 79% of private investors plan to increase their allocations, driven by a desire for diversification and access to the “real economy.”

This demand is fuelling the proliferation of “evergreen” or semi-liquid funds. These structures, designed to offer periodic liquidity and lower minimums, are becoming a critical source of steady capital for GPs.

Figure 2: Number of Evergreen Funds

Growth in the number of evergreen and semi-liquid private market vehicles

Source: Blackrock, 2025

For institutional LPs, this trend is a double-edged sword: it deepens the capital pool but potentially introduces new volatility if retail flows reverse during market stress.

The democratisation of private markets will succeed only where access is matched by governance, transparency and realistic liquidity expectations.

Partners Group, Private Markets Outlook 2026

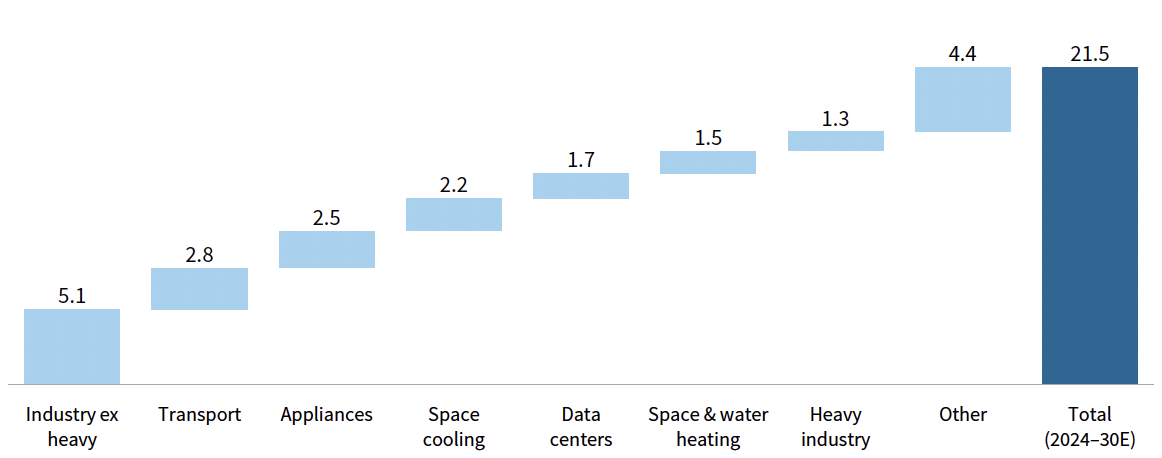

AI as a physical asset theme

The conversation around Artificial Intelligence (AI) has moved beyond software valuations to physical reality. The consensus across outlooks is that the immediate, investable opportunity lies in the infrastructure required to train and run AI models. This is a capital-intensive game involving data centres, power generation and grid upgrades.

BlackRock and Partners Group both emphasise that the energy demand of AI is colliding with the energy transition, creating a massive need for capital that governments alone cannot provide.

This convergence is generating opportunities for infrastructure and real estate investors to build the “picks and shovels” of the AI revolution, assets that offer potential downside protection through long-term contracts, unlike the volatile equity of pure-play AI tech firms.

Figure 3: Global electricity demand growth drivers

Source: Cambridge Associates, 2025

Asset-class analysis

Private Equity

Private equity is entering an era of execution. The days of relying on multiple expansion and cheap leverage are over. Adams Street and Partners Group both highlight that future returns must come from operational improvements – revenue growth, margin expansion and strategic platform building.

- Investment Activity: Dealmaking is rebounding from the lows of 2023–2024, driven by corporate carve-outs and take-privates. However, buyers remain disciplined, wary of overpaying in a “high altitude” valuation environment.

- Valuations: Entry multiples remain sticky, particularly for high-quality assets in resilient sectors like software and healthcare. This leaves little room for error; managers must have high conviction in their value-creation plans.

- Exits: The exit environment remains the primary bottleneck. While there are green shoots in the IPO market, they are insufficient to clear the backlog of unexited assets. GPs are increasingly reliant on “manufactured” exits – sales to other sponsors and continuation vehicles – to return capital to LPs.

The next phase of private equity returns will be earned through operational execution, not financial engineering.

Partners Group, Private Markets Outlook 2026

Private Credit

Private credit has matured into a permanent fixture of corporate finance, but the “golden age” of easy excess returns may be normalising. As spreads compress, particularly in the upper middle market, the asset class is bifurcating.

- Core Middle Market: Lenders are retreating to the core middle market, where competition is less fierce, covenants remain stronger, and spreads are wider compared to the large-cap space.

- Asset-Based Finance (ABF): A major theme for 2026 is the rotation into ABF – lending against pools of assets like consumer loans, equipment or intellectual property. Apollo highlights this as a multi-trillion-dollar opportunity that offers diversification away from corporate credit risk and correlation.

- Risks: Defaults remain low but are a lagging indicator. The key risk is not systemic collapse but “liability management exercises” (LMEs) where sponsors aggressively restructure debt at the expense of lenders.

Private credit has evolved from an alternative allocation into a core component of corporate financing.

Ares Management, Private Credit Outlook 2026

Infrastructure

Infrastructure is increasingly viewed as the “star” asset class for the coming decade. It sits at the intersection of the world’s most powerful secular trends: digitalisation, decarbonisation and deglobalisation.

- Themes: The focus is shifting from traditional GDP-linked assets (roads, airports) to “digital infrastructure” (data centres, fibre) and the energy transition (renewables, grid storage).

- Returns: Investors are attracted to the asset class for its inflation linkage and defensive characteristics. However, with valuations for high-quality assets rising, there is a push towards “value-add” strategies where managers take on development risk to generate higher returns.

AI-driven power demand and energy security are reshaping the long-term infrastructure investment landscape.

Allianz Global Investors, Outlook 2026

Real Estate

Real estate is showing signs of stabilising after a painful correction, but the recovery is uneven. Goldman Sachs asks if the sector is “ready for a rebound,” suggesting that clarity on peak rates may finally unlock transaction volumes.

- Bifurcation: The divide between “haves” and “have-nots” is extreme. Industrial logistics and residential sectors benefit from structural tailwinds (e-commerce, housing shortages) and rental growth.

- The Office Problem: The office sector remains distressed, with vacancy rates in the US significantly higher than in Europe or Asia. LPs are largely avoiding the sector, focusing instead on niche areas like data centres, which have crossed over from infrastructure into real estate portfolios.

Venture Capital

Venture capital is stabilising after a severe correction. The “growth at all costs” mentality has been replaced by a focus on unit economics and path to profitability. While AI remains the dominant theme attracting capital, Cambridge Associates warns investors to “find value amid the hype,” advising caution around inflated seed-stage valuations and suggesting a more selective approach to manager exposure.

Venture capital is transitioning from an era of excess to one where capital efficiency and governance matter as much as growth.

Cambridge Associates, 2026 Outlook

LP lens

The themes of 2026 demand a shift in LP behaviour. The passive “commitment pacing” models of the past decade – where LPs steadily deployed capital into the same vintage years of the same managers – are being challenged by the liquidity crunch. LPs are becoming more active managers of their own balance sheets.

The denominator effect has forced LPs to become liquidity providers to their own portfolios. We are seeing LPs utilising the secondary market not just to sell tail-end funds, but to actively prune concentrated positions or exit managers who are not returning capital. There is also a growing demand for transparency.

LPs are scrutinising DPI over TVPI (total value) and are increasingly sceptical of unrealised mark-to-market gains that do not translate into cash.

Governance is becoming a flashpoint. As GPs turn to continuation vehicles to hold assets longer, LPs are facing complex conflicts of interest. They are being asked to “re-underwrite” assets they already own, often with short timelines and limited information.

This requires LPs to upgrade their internal capabilities or lean more heavily on consultants to navigate these transactions.

Key LP concerns and fault lines

Valuation Integrity: There is a persistent, quiet tension regarding private market valuations. While public markets adjusted sharply in 2022-2023, private marks were “smoothed.” LPs remain sceptical that older vintages (2020-2022) are marked accurately, fearing that embedded losses have yet to be crystallised.

The “DPI” Crisis: The single biggest friction point is the lack of distributions. LPs operate on cash flow; they need distributions to fund liabilities and new commitments. The “numerator problem” – where the value of private assets remains high but the cash isn’t there – is forcing LPs to make hard choices, including cutting commitment sizes or selling high-quality assets in the secondary market to generate liquidity.

Leverage on Leverage: The rise of NAV loans (borrowing against the net asset value of a fund) to generate distributions or support portfolio companies is a growing concern. LPs are wary of “synthetic” DPI – where GPs borrow money to pay distributions – viewing it as financial engineering that adds risk without creating value.

Alignment of Interest: The explosion of continuation vehicles has raised fundamental questions about alignment. When a GP sits on both sides of the table – selling an asset from Fund V to Fund VI – LPs question whether the price and terms are truly fair, or if the process is designed to generate fees rather than maximise returns.

What this means for allocations

Be Active, Not Passive: The “set it and forget it” era is over. LPs must actively manage their portfolios, using secondaries to create liquidity and rebalance. This might mean selling decent assets to buy great ones, or selling older vintages to free up capacity for fresh commitments.

Diversify Vintage Risk: Despite the liquidity crunch, LPs are advised not to stop committing. History shows that vintages investing during periods of dislocation (like 2025-2026) often produce the best returns. The key is to maintain consistent pacing, even if check sizes must be smaller.

Lean into Secondaries: Secondaries are highlighted as a tactical overweight. They offer a unique combination of J-curve mitigation (immediate exposure to funded assets), diversification and potential discounts. For LPs facing liquidity constraints, secondaries offer a way to put money to work that comes back faster.

Look at Asset-Based Finance: For fixed income and credit allocations, consider rotating capacity from corporate direct lending into asset-based finance. This segment offers diversification away from corporate credit risk, often with better collateral protection and uncorrelated cash flows.

Scrutinise the “Value Creation” Playbook: When evaluating PE managers, dig deep into their operational capabilities. How exactly do they plan to grow EBITDA? If the answer relies on “multiple arbitrage” or “cheap debt,” move on. Look for sector specialists with large operating benches who can drive genuine business transformation.

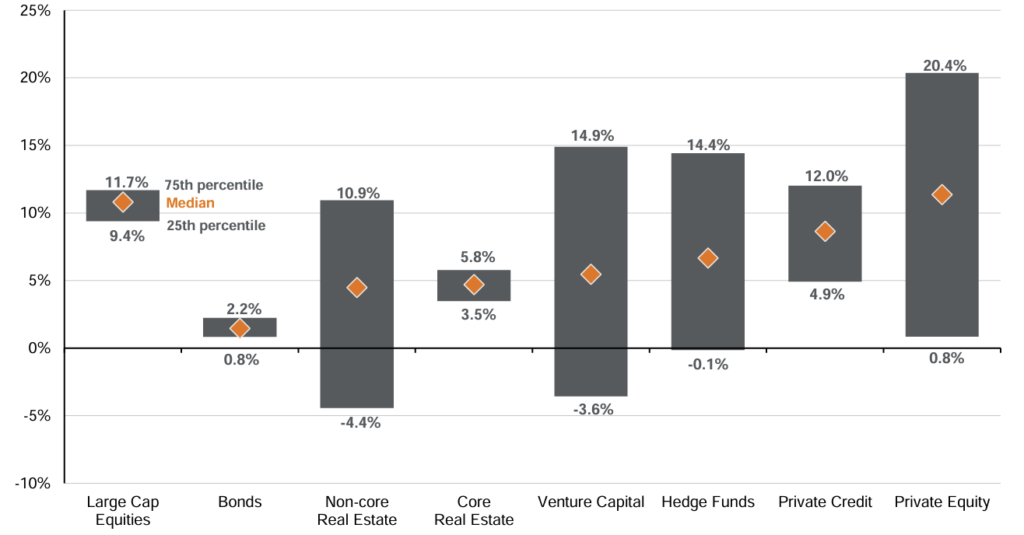

CIO takeaway

For Chief Investment Officers, 2026 is a year for disciplined dynamism. The era of rising tides lifting all boats is over; we are now in a stock-picker’s market where manager dispersion will determine success.

Figure 4: Return dispersion across public and private asset classes (3Q15 – 3Q25)

Return dispersion across public and private asset classes (3Q15–3Q25). Interquartile return ranges highlight widening dispersion across asset classes, reinforcing the importance of manager selection, governance and underwriting discipline in portfolio construction.

Source: J.P. Morgan Asset Management, 2025.

Do not retreat from private markets, but demand more from them. Prioritise managers who demonstrate a clear path to liquidity and operational value creation. Use the secondary market as a strategic tool, not a distress valve.

Finally, ensure your governance processes are robust enough to handle the increasing complexity of GP-led transactions and new fund structures. The portfolio of the future is not just allocated; it is actively managed.

Final thoughts

The private markets industry is proving its resilience, but it is undergoing a fundamental metabolic change. The “sugar rush” of cheap capital has faded, replaced by the harder, healthier work of building better businesses. For LPs, this transition is painful – marked by liquidity constraints and difficult decisions – but ultimately healthy.

Success in 2026 will not come from simply being allocated to the asset class. It will come to those who can distinguish between financial engineering and genuine value creation, and who have the agility to navigate a more complex, bifurcated and demanding investment landscape. The free lunch is over; it’s time to cook.

Stay Illiquid!

Kasper

Sources

- Adams Street Partners: Private Markets 2026 Outlook

- Apollo Global Management: Outlook for private markets

- Barclays Private Bank: Private Markets Annual Report 2025

- BlackRock: Private Markets Outlook 2026

- Cambridge Associates: 2026 Outlook: Finding Value Amid the Hype

- Goldman Sachs Asset Management: Private Markets and Alternatives Outlook 2026

- J.P. Morgan Asset Management: Guide to Alternatives

- Partners Group: Private Markets Outlook 2026

More Insights

Balentic Edge

Sign up to keep up to date with the latest news and updates.

© 2025 Balentic ApS. CVR: 44034255. All rights reserved.

Privacy Policy | Terms of Service

The Balentic website and Orca are, and are expected to continue to be, under development. Consequently, some of the features described in this Overview and/or on the website may not yet be available or may work differently. Some features may furthermore not be available to all users.