Why Some Clubs Turn Money Into Trophies, and Others Into Excuses

What do Liverpool, Real Madrid and the best private markets managers have in common? More than most LPs might think. This is the second part of It Might Be Easier to Predict the Champions League Winner Than Private Markets Returns.

Last week, Paris Saint-Germain booked their place in another Champions League final.

Had that happened five years ago, the explanation would have written itself. Qatar’s money. A limitless wage bill. Another example of football’s financial arms race overwhelming the sport’s competitive balance.

Today, the story feels rather different.

This PSG side is younger, more cohesive and considerably less dependent on superstar individuals than the versions built around Neymar, Messi and Mbappé. Under Luis Enrique, PSG increasingly resembles a football club rather than a collection of footballers. The wage bill remains substantial, of course, but the emphasis has shifted from assembling talent to building a team.

That distinction matters.

Because while money undoubtedly influences success in football, it explains far less than many assume. If wages alone determined outcomes, the Champions League would be little more than an accounting exercise. The club with the largest payroll would simply collect its trophy in May and everyone else could save themselves the trouble.

Instead, football thankfully persists in being football.

The best-funded clubs tend to reach the latter stages of the competition, but, as we saw in Part 1, they do not all get there with the same frequency. Some consistently convert resources into results. Others consistently fall short of what those resources ought to deliver.

The same phenomenon exists in private markets.

Access to capital matters. Scale matters. Brand matters. Yet anyone who has spent enough time around fund managers knows that these things are not the same as performance.

Some firms seem capable of producing strong outcomes across cycles and market conditions. Others raise larger funds, attract greater attention and still struggle to deliver comparable results.

Part 1 explored why it may be easier to identify structural winners in football than in private markets. The Champions League, despite its reputation for unpredictability, reveals a surprisingly concentrated group of repeat contenders. Private markets, by contrast, offer much less persistence at the strategy level.

The obvious question is why.

The answer begins with money, but it does not end there.

Executive Summary

- Wage bills help explain who reaches the Champions League, but they do not fully explain who wins it

- Some clubs consistently convert resources into results more effectively than their peers, suggesting the presence of structural advantages

- Luck and timing influence individual outcomes, but persistent success is more often the product of recruitment, culture, leadership and institutional quality

- The same distinction exists in private markets, where fundraising success, scale and brand recognition do not necessarily translate into superior performance

- For LPs, the challenge is not simply allocating capital, but identifying the organisations that repeatedly convert opportunity into results

“Everybody says it's (success) being in the right place at the right time. But it's more than that. It's being in the right place all the time.”

Gary Lineker

The Limits of Financial Determinism

Football’s relationship with money has always attracted strong opinions.

Supporters of smaller clubs often point to wage bills as evidence that success has been bought. Supporters of larger clubs tend to argue that spending is simply a reflection of ambition and competence. Both views contain some truth, and neither fully explains what happens on the pitch.

The relationship between wages and Champions League performance is real and measurable. Clubs with larger payrolls generally perform better than those with smaller ones. That should surprise nobody. Better players command higher salaries, and in a weak link type of sport, having the better players tends to winning more matches.

Yet the relationship is far from perfect.

The wage versus performance analysis reveals a pattern that should look familiar to any LP reviewing a portfolio of fund managers.

Some clubs perform broadly in line with expectations. Others consistently exceed them. A third group repeatedly falls short.

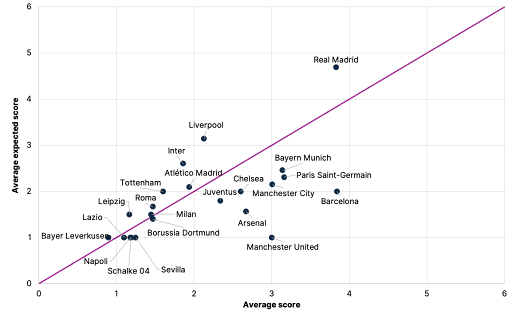

Chart 1: Wage Bills Explain Access. They Do Not Fully Explain Outcomes

Average Champions League performance versus average wage-derived expectation. Clubs above the line outperform expectations. Clubs below it underperform them.

The interesting observations are rarely found at the extremes.

No one is shocked when Real Madrid reaches the latter stages of the Champions League. Equally, nobody expects a modestly funded club to dominate European football year after year.

The more revealing cases sit in the middle.

Liverpool have spent much of the last decade competing with clubs that possessed equal or greater financial resources. Yet they repeatedly appeared in the latter stages of the competition and converted those appearances into trophies.

Atlético Madrid has spent years operating in the shadow of both Real Madrid and Barcelona, while regularly outperforming what its wage bill might imply – notwithstanding Diego Simeone, who supposedly is the highest paid manager in football.

Inter have navigated periods of financial constraint while remaining surprisingly competitive.

These clubs differ in history, geography and ownership structure. What they share is an ability to extract more value from their resources than many of their peers.

In private markets, investors often describe this as execution.

In football, we tend to call it winning.

The distinction is largely semantic.

The Clubs That Refuse to Behave as Expected

One of the more revealing findings from the analysis is that some clubs seem remarkably resistant to regression.

Over a single season, almost anything can happen. A favourable draw, a contentious refereeing decision, an untimely injury or a moment of brilliance can alter the trajectory of a campaign. Football is emotional precisely because it contains a degree of randomness. Remove that uncertainty and much of the appeal disappears with it.

Yet over longer periods, luck becomes a less satisfying explanation.

Liverpool’s success over the past decade cannot be attributed to a handful of fortunate moments. Nor can Atlético Madrid’s repeated ability to compete with clubs possessing significantly greater resources. The same applies to Inter and, increasingly, to clubs such as RB Leipzig.

Different clubs. Different ownership structures. Different leagues.

The common factor is not luck.

It is the ability to repeatedly convert resources into outcomes.

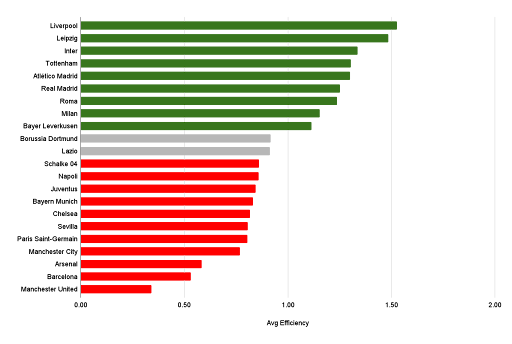

The efficiency rankings attempt to measure precisely this phenomenon. Rather than asking which clubs achieve the most, they ask which clubs achieve the most relative to what should reasonably be expected.

Overall the view, also backed by data, was the election of a Democrat or a Republican had historically had little notable effect on private markets. But it was also pointed out that the policies of the two candidates today do differ substantially and that for example green’ industries would in the case of a Democratic victory likely benefit, which would likely not be the case with a Republican victory.

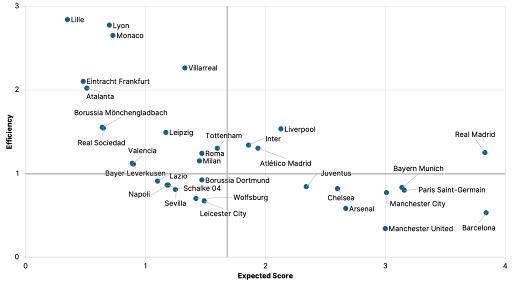

Chart 2: Some Clubs Consistently Convert Resources Into Results More Effectively Than Others

Average efficiency measures performance relative to wage-derived expectations across Champions League campaigns.

That distinction is important.

Success is often mistaken for quality. The two are related, but they are not identical.

A club with one of the largest wage bills in Europe should be expected to reach the latter stages of the Champions League. When it does, it has fulfilled expectations. When a club operating with fewer resources achieves the same outcome, something more interesting may be taking place.

This is where Liverpool becomes particularly instructive.

Throughout much of the period under review, Liverpool operated with resources that were substantial but not dominant. Manchester City, Paris Saint-Germain, Barcelona and Real Madrid frequently possessed greater financial firepower. Yet Liverpool consistently found ways to remain competitive at the highest level.

Supporters will point to different explanations. Jurgen Klopp. Recruitment. Culture. Anfield. All contain elements of truth.

More broadly, however, Liverpool represents an organisation that developed a coherent operating model and applied it consistently over time. Recruitment aligned with strategy. Coaching aligned with recruitment. The institution functioned as a system rather than a collection of individual decisions.

The same observation can be made about Atlético Madrid.

For more than a decade, Diego Simeone built a team capable of competing against opponents with greater resources. Atlético did not win every year. No club does. What they achieved was arguably more impressive. They remained relevant year after year in an environment designed to favour richer competitors.

That consistency is difficult to fake.

Private markets offers similar examples.

Every LP has encountered managers who seem capable of generating strong outcomes regardless of market conditions. Their strategies evolve. Teams change. Cycles come and go. Yet performance remains remarkably resilient.

The explanation is rarely a single investment decision.

It is usually the product of an organisation that understands what it is trying to achieve and possesses the discipline to execute against that objective repeatedly.

The challenge, of course, is distinguishing these organisations from those that merely appear successful during favourable conditions.

That brings us to the opposite side of the equation.

Because some of the most interesting observations emerge not from the clubs that do more with less, but from those that do less with more.

The Dangerous Illusion of Scale

There is a tendency, in both football and investing, to assume that resources eventually solve most problems.

Given enough money, success becomes inevitable.

History suggests otherwise.

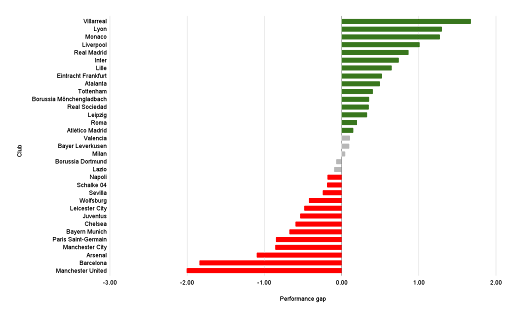

Chart 3: Some Clubs Underperform Expectations at Scale

Average efficiency measures performance relative to wage-derived expectations across Champions League campaigns.

This very likely for good, and should, if not already the case, should prompt LPs to:

Manchester United remains one of the most successful and recognisable football clubs in the world. Its global following is enormous. Its revenues remain among the highest in the game. Yet for much of the past decade, basically since Alex Ferguson left, the club has appeared rudderless and struggled to translate those advantages into consistent Champions League success.

This is not a story about a lack of resources.

It is a story about what happens when resources are deployed without sufficient organisational coherence.

The challenge is not unique to football.

Many investment organisations experience something similar as they scale. Teams expand. Assets under management grow. New products are launched. Success creates complexity, and complexity often creates friction.

What once felt focused begins to feel bureaucratic. Decision-making slows. Accountability becomes diffuse. Performance suffers. The dressing room splinters.

The relationship between scale and quality becomes weaker than many assume.

This is one reason the modern evolution of Paris Saint-Germain is so interesting.

For years, PSG served as the preferred example for critics of football’s financial excesses. The club assembled extraordinary talent and achieved almost unparalleled domestic success yet repeatedly fell short in Europe.

The current side feels very different.

The resources remain substantial, but the emphasis has shifted from individual star power towards collective effectiveness. Last year, with a victory over Inter, that finally led to a first Champions League title. Whether they will repeat the same feat tomorrow by possibly beating Arsenal remains uncertain. Football, thankfully, retains the capacity to surprise.

What matters is that the club increasingly resembles an institution rather than a marketing strategy.

The distinction may sound subtle. It is not.

The same transition occurs in private markets. The strongest firms eventually evolve beyond individual rainmakers and star dealmakers. They become organisations capable of producing outcomes systematically rather than episodically.

Not every firm manages the transition successfully.

Not every club does either.

Luck, Timing and the Myth of Meritocracy

At this point, football supporters will reasonably object.

Real Madrid’s recent history includes late goals that seemed to defy probability. Liverpool have benefited from favourable moments. Manchester City have suffered painful exits decided by fine margins. Referees make mistakes. VAR intervenes. Crossbars are struck. Penalties are missed.

Football, after all, is football – luck matters.

Private markets are no different. A fund launched six months earlier or later can experience a very different market environment. A refinancing window opens unexpectedly. Interest rates move. A geopolitical event changes an investment thesis overnight. Two managers can make broadly similar decisions and produce materially different outcomes.

Anyone who claims otherwise has probably spent too much time reading their own marketing materials.

There can therefore be a temptation to conclude that outcomes are largely a function of chance.

That conclusion is understandable, but it is also incomplete.

The problem with focusing on individual events is that they explain specific outcomes but struggle to explain recurring patterns.

Luck can help a club win a match.

It is less effective at explaining why certain clubs repeatedly find themselves competing for the trophy.

Likewise, luck can influence the outcome of a particular investment, a particular fund, or even a particular vintage – as an example Defense, which benefits from an almost once in a generation type of tailwind, comes to mind.

But luck becomes a much weaker explanation when the same organisations continue to produce strong outcomes over long periods of time.

The distinction is subtle but important.

Luck influences outcomes.

Structure influences the probability of outcomes

The clubs that consistently reach the latter stages of the Champions League are not immune to vagaries of lady luck. They simply create more opportunities for the lady to favour them.

A team that reaches ten quarter-finals will inevitably benefit from a favourable bounce of the ball at some point. Equally, it will suffer from an unfavourable one.

But, over time, those events tend to wash out. What remains is the ability to repeatedly place oneself in contention.

The same logic applies to investing.

Some managers seem perpetually lucky – the GP equivalent of “Fergie-time”. Their investments work. Their exits arrive at favourable moments. Their portfolios appear unusually resilient.

Eventually, one begins to suspect that something other than luck may be involved.

Not because chance disappears, but because well-constructed organisations consistently create conditions in which chance can be exploited.

The distinction is perhaps best illustrated through the relationship between preparation and opportunity.

When Liverpool identify and develop players before competitors recognise their value, that is not luck.

When Atlético Madrid repeatedly assemble squads capable of competing above their apparent financial weight, that is not luck.

When a private markets manager develops sourcing networks, maintains investment discipline through market cycles, and builds a culture that survives changes in personnel, that is not luck either.

Yet all three increase the likelihood that favourable opportunities can be recognised and acted upon when they emerge.

In hindsight, we often describe such outcomes as fortunate. In reality, they are frequently the product of years of preparation.

The danger for investors is that outcomes are far easier to observe than processes.

Trophies are visible.

Returns are visible.

The decisions that created them often are not.

This creates a natural bias towards judging organisations by what happened rather than how it happened.

In football, that tendency produces endless debates about managers, transfers and individual matches.

In private markets, it produces an equally endless fascination with recent performance rankings – the unhealthy obsession with benchmarks and IRRs.

Neither necessarily tells us very much about future success.

The more useful question is whether an organisation possesses characteristics that increase its probability of success over time.

That is a harder question to answer, but it is also the only one that matters. Because the objective for an LP is not to identify managers that have been fortunate.

It is to identify managers that have built institutions capable of benefiting from good fortune when it arrives and surviving bad fortune when it does not.

That is a very different challenge.

And it brings us to the central lesson from both football and investing.

The most valuable capabilities are often the least visible.

Capital Matters. Institutions Matter More.

The temptation in both football and investing is to focus on outcomes.

Trophies. Returns. League tables. Rankings.

These are the visible markers of success. They are easy to measure, easy to compare and easy to discuss. They are also, in many respects, the least interesting part of the story.

What matters is how those outcomes were produced.

Chart 4: The Difference Between Resources and Execution

Average efficiency measures performance relative to wage-derived expectations across Champions League campaigns.

The Champions League offers a useful reminder of this distinction. From a distance, success appears to follow resources. The clubs with the largest wage bills generally progress furthest. Money clearly matters.

Yet the analysis suggests that money explains less than many assume.

Some clubs consistently convert resources into results. Others consistently fail to do so. The difference is rarely explained by a single transfer, a single manager or a single season. Instead, it emerges from a collection of decisions that compound over time.

Recruitment. Culture. Leadership. Incentives. Stability. Process.

These are not particularly glamorous topics. They do not generate headlines or social media engagement. They are also the foundations upon which enduring success is built.

Private markets are no different.

Investors often spend considerable time debating asset allocation. Should exposure be increased to buyout? Is private debt becoming too crowded? Has venture capital become investable again? These are important questions, but they are not always the most consequential ones.

The more difficult challenge is identifying organisations that consistently transform resources into outcomes.

The strongest managers rarely look exceptional because of a single investment. They look exceptional because they repeatedly make good decisions, attract talented people, maintain discipline through changing market conditions and preserve their culture as they grow.

In other words, they become institutions.

This is also why scale can be deceptive.

Fundraising success does not necessarily indicate investment skill. Assets under management do not automatically translate into performance. Access to capital does not guarantee superior outcomes.

In football, we instinctively understand this distinction. In private markets, we are sometimes reluctant to acknowledge it.

Football provides countless examples of clubs that possessed every conceivable advantage and still fell short. Private markets offers its own versions of the same story.

Conversely, some organisations consistently outperform despite lacking the largest budgets, the highest profile or the greatest resources.

Over time, these are often the organisations that matter most.

None of this implies that luck is irrelevant.

A refereeing decision can change a football match. A market dislocation can transform the fortunes of an investment. Timing, circumstance and chance influence outcomes in both worlds.

Yet over longer periods, luck tends to amplify preparation rather than replace it.

The clubs that repeatedly reach the latter stages of the Champions League are not necessarily the luckiest. They are the clubs that most consistently place themselves in positions where luck can make a difference.

The same is true of successful investment organisations.

Which brings us back to the central lesson

The objective is not to identify who won yesterday. It is to understand why they keep winning.

For LPs, that means looking beyond recent returns and headline performance – which in fact is written again and again in every single manager presentation “past performance is not a predictor of future returns”.

Instead it means understanding organisational quality, investment process, decision-making structures and cultural durability. It means recognising that the most important drivers of future performance are often hidden beneath the outcomes that receive the most attention.

The Champions League may be more predictable than private markets.

But both reward the same thing.

Not capital alone.

Not talent alone.

Not luck alone.

The ability to repeatedly convert opportunity into results.

Capital matters.

Talent matters.

Luck matters.

But institutions matter most.

Stay Illiquid

Kasper

Sources

- UEFA Champions League historical data

- Deloitte Football Money League

- Transfermarkt

- FBref

This article is provided for informational purposes only and does not constitute investment advice, legal advice, or a recommendation to buy or sell any security, financial instrument, or investment strategy. Nothing herein constitutes an offer or solicitation in any jurisdiction. Any references to investment strategies, market activity, or participants are illustrative and do not imply the availability of any investment opportunity. The content is not directed at retail investors. Where applicable, access to investment-related information is restricted to professional or institutional investors under relevant laws and regulations, including but not limited to Regulation D under the U.S. Securities Act of 1933, the EU Alternative Investment Fund Managers Directive (AIFMD), and the UK Financial Promotion Regime (COBS 4). Views expressed are those of the author(s) and may change without notice.

More Insights

Balentic Edge

Sign up to keep up to date with the latest news and updates.

© 2025 Balentic ApS. CVR: 44034255. All rights reserved.

Privacy Policy | Terms of Service

The Balentic website and Orca are, and are expected to continue to be, under development. Consequently, some of the features described in this Overview and/or on the website may not yet be available or may work differently. Some features may furthermore not be available to all users.